Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

The network infrastructure market is the foundation of the digital economy – encompassing hardware, software and services that provide connectivity and data exchange on a global scale. The dynamic development of mobile technology, cloud computing and the Internet of Things (IoT) is driving investment in modern networks. As a result, network infrastructure is undergoing intense modernisation: telecom operators are deploying 5G, companies are migrating to the cloud and the hybrid working model, and organisations are betting on network automation. This article analyses the current value of the global network infrastructure market, its growth forecasts, regional differentiation, key technology trends (5G, edge computing, SD-WAN, AI) and key market players. It also provides an expert assessment of the outlook for the next 5-10 years and the key challenges – from costs to security to problems with outdated systems.

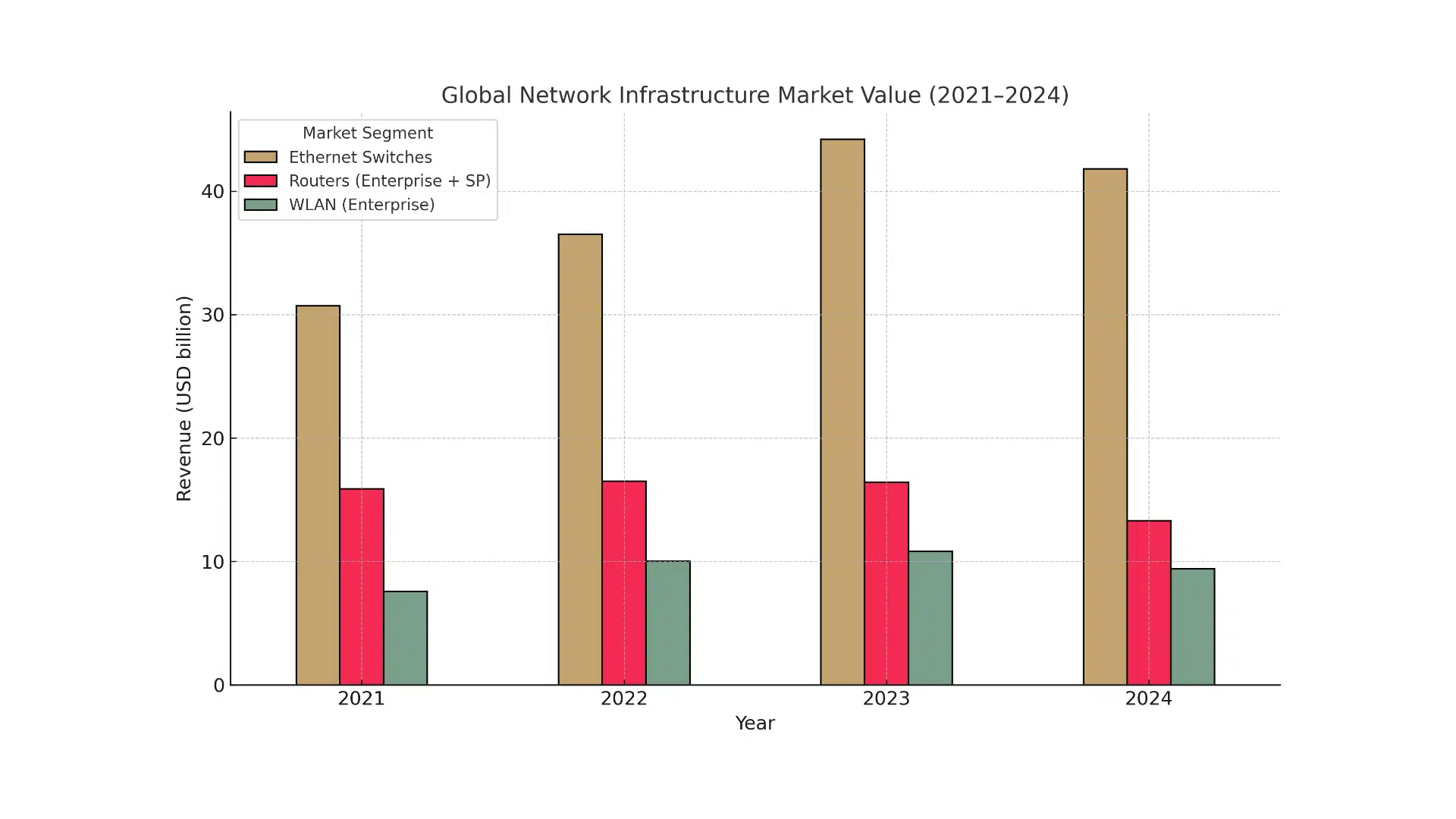

The global network infrastructure market is worth hundreds of billions of dollars and is showing steady growth. Its value reached around USD 248.8 billion in 2024 and is forecast to grow to USD 463.9 billion in 2033. This means that the market will grow at a compound annual growth rate (CAGR) of around 7.2 per cent on average between 2025 and 2033. Such growth reflects the increasing demand for advanced networking technologies around the world – from data centre modernisation, cloud and 5G integration to the development of smart cities. Demand is driven by both the private sector (digital transformation of businesses) and public investment in broadband and mobile infrastructure.

In 2024, the market was valued at just under USD 250 billion, to almost double its value to around USD 464 billion by 2033. The growth trend is relatively uniform and stable – reflecting the maturity of the market and the continued organic growth in demand for network capacity, security and new functionality. Importantly, the structure of the market includes network hardware (around 48% market share) and network software and services (together the remaining 52%), which means that, in addition to investment in physical equipment, the role of software solutions that define network operations is growing.

Network infrastructure is growing in all regions of the world, but the dynamics and scale of investment vary by area. Asia and the Asia-Pacific region currently represent the largest segment, accounting for around 34% of the global market and showing the fastest growth rate. The main driver here is the expansion of next-generation mobile networks and urbanisation: it is estimated that more than half (51%) of all 5G base stations worldwide are located in Asia-Pacific. Countries such as China, Japan, South Korea and India are leading the way with investments in 5G and smart city projects. For example, some 68% of enterprises in the APAC region are betting on migrating to the cloud, and 59% are deploying advanced industrial networks for smart manufacturing and urban infrastructure.

North America accounts for approximately 31% of the value of the global market and remains at the forefront of deploying the latest network solutions. The US accounts for the lion’s share of this market, with approximately 84% of North American infrastructure investment occurring in the US. The region has the highest density of data centres, widespread fibre availability and a rapid pace of 5G deployment. Already 48% of organisations in North America are using 5G connectivity in their operations. In addition, companies are placing a strong emphasis on security, with nearly 69% of US companies prioritising the integration of cyber security into their network infrastructure. Government programmes supporting network expansion and the widespread digitisation of business are also contributing to the growth.

Europe accounts for approximately 27% of the global network infrastructure market. With key markets in Germany, the UK and France, the region is focusing on modernising corporate and telecom networks based on software-defined networking architectures. Already, some 61% of European enterprises are deploying SDN (Software-Defined Networking) solutions and 58% are investing in multi-cloud strategies – integrating multiple clouds for greater flexibility. European operators and companies are also intensively developing data centre infrastructure and fibre networks, preparing the ground for 5G rollout and future 6G deployments around the end of the decade. Despite a slightly smaller share of the global market, Europe maintains high standards of security and interoperability and is paying increasing attention to the energy efficiency of infrastructure – some 31% of new network investments in Europe and Asia are already directed towards green, energy-efficient technologies.

Other regions are also seeing growth: The Middle East and Africa together account for around 8% of the market, catching up through digital infrastructure projects often funded by government funding and public-private partnerships. Latin America, meanwhile, is investing in the expansion of 4G/5G and fibre networks, although the scale of spending there is smaller compared to the three main regions.

Several key technology trends are clearly emerging in the network infrastructure that are shaping the development of the market:

The network infrastructure market is dominated by a handful of large global vendors who compete in both the telecoms equipment and corporate network solutions segments. These include Cisco, Huawei, Nokia and Ericsson, among others:

In addition to those mentioned, there are other major players in the network infrastructure market specialising in selected areas – including ZTE, Juniper Networks, Arista Networks, Dell EMC, HPE (Aruba), Extreme Networks or CommScope. The aforementioned companies compete in segments such as data centre switches, campus LAN/WLAN equipment, cabling or cloud solutions, completing the global network infrastructure ecosystem.

According to experts, the growth prospects for the network infrastructure market over the next 5-10 years remain very promising. A projected average annual growth rate of 7% means that the sector will grow faster than many traditional industries, although slightly slower than the most dynamic segments of the IT market. The key technology trends described above will continue to drive investment: the global roll-out of 5G (and, looking ahead to the end of the decade, the first 6G deployments) will ensure continued demand for equipment and operator network upgrades. Edge computing will become an integral part of the network architecture – more and more data will be processed locally, creating a demand for distributed network nodes close to the user. Cloud and multicloud solutions will force the construction of networks capable of handling dynamic, distributed workloads, fostering the development of intelligent, software-defined networks. Automation using AI is likely to transform the way networks are managed – we are already seeing a trend towards autonomous networks, able to optimise traffic and respond to incidents autonomously. In the long term, this could result in significant operational savings and improved security.

Regionally, the current balance of power is expected to continue, with Asia-Pacific remaining the largest and fastest-growing market due to investment in China and developing countries, North America maintaining high levels of innovation and corporate spending (especially in the US), and Europe consistently upgrading infrastructure with a focus on security and efficiency. However, the disparity between regions may narrow as network technologies become ubiquitous and deployment costs fall.

Experts also highlight new areas of growth that may become increasingly important: private 5G networks for enterprises (e.g. in factories, ports or university campuses), networks for IoT supporting billions of devices (including narrowband LPWAN networks for sensors) or the development of the satellite internet (e.g. constellations in low orbit providing global connectivity). The digital transformation of sectors such as energy (smart grid), automotive (connected vehicles) or medicine (telemedicine, wearable devices) will generate demand for a reliable communication infrastructure. A further increase in research and development (R&D) spending in the network area can be expected – both by market giants and new players (startups), which will result in further innovations and even more efficient network technologies in the future.

Despite the positive outlook, the global network infrastructure market faces several significant challenges. The biggest barrier is high cost – network upgrades require huge capital expenditure. More than 44% of enterprises cite budget constraints as a factor inhibiting infrastructure upgrades. Next-generation hardware (e.g. 5G devices, backbone routers, edge nodes) and associated software and integration are costly investments that not all organisations can afford immediately. At the same time, obsolete (legacy) systems are still common – it is estimated that around 27% of the network infrastructure in use globally is made up of older, previous-generation equipment. Migrating from these legacy systems is difficult: nearly 38% of companies struggle to replace old hardware with newer hardware. Maintaining such solutions raises not only opportunity costs (lower performance, lack of new features), but also security risks – almost 33% of security breaches are related to vulnerabilities in outdated infrastructure.

Cyber security is itself another challenge. The increasing complexity of networks (especially those distributed across multiple clouds and locations) means that 59% of organisations find it difficult to manage security in multicloud and hybrid environments. Attacks on network infrastructure are increasing in sophistication and the attack surface is widening with the connection of more IoT devices and the proliferation of 5G networks. Ensuring consistent security policies, network segmentation and data protection in such a heterogeneous environment is a heavy burden for IT departments. Many companies also face staff shortages, with some 29% of enterprises citing a shortage of qualified advanced network professionals as a limiting factor to progress.

Another challenge is interoperability and integration of new technologies with existing infrastructure. Companies often use multi-vendor solutions, which raises compatibility issues. More than 34% of organisations experience integration issues when deploying disparate platforms and services. Standardisation of protocols and openness of ecosystems are therefore becoming crucial to avoid technology silos. Additionally, regulators are imposing requirements on the industry (e.g. on cyber security, data privacy or spectrum allocation), which can slow down deployments, especially in the telecoms sector.